Those whom the gods wish to destroy they first send mad

Introduction

The aim of this article is to show that the shale industry, whether extracting oil or gas, has never been financially sustainable. All around the world it has consistently disappointed profit expectations. Even though it has produced considerable quantities of oil and gas, and enough to influence oil and gas prices, the industry has mostly been unprofitable and has only been able to continue by running up more and more debt. How could this be? It seems paradoxical and defies ordinary economic logic. The answer is to be found in the way that the shale gas sector has been funded. It is part of a bubble economy inflated by monetary policy that has kept down interest rates. This has made investors “hunt for yield”. These investors believed that they had found a paying investment in shale companies – but they were really proving that they were susceptible to wishful thinking, vulnerable to hype and highly unethical practices that enabled Wall Street and other bankers to do very nicely. Those who invested in fracking are going to lose a lot of money.

A Global Picture of disappointed expectations

Around the world big expectations for fracking have not been realised. One example is Argentina where shale oil reserves were thought to rival those in the USA. It is a country where there has been local opposition while central government pushed the industry in alliance with multinational companies and its own company YPC. However profitability has been elusive. To have any hope of profitability shale development has to be done at scale to rapidly bring down costs enough to make a profit. That requires a lot of capital and companies will not make this capital available without being sure that they are going to make a lot of money – but they cannot be sure until they have done tests for up to two years.

“It’s a sort of chicken and egg dilemma. Without profits, the estimated $20 billion a year needed to develop the play won’t come. And without this investment in drilling tens of thousands of wells, the economies of scale won’t be reached on the fields to cut costs.

“A reason not to rush into production — only 400 wells have been drilled — is that wells must be tested for up to two years to gauge the potential of the shale rock before a company will commit billions of dollars. This is especially the case now that low global oil prices have slimmed investment budgets for frontier plays.” (Charles Newbury, “Struggles to cut cost delay oil production in Argentina” Platts Oilgram News. August 17th 2015 at http://blogs.platts.com/2015/08/17/cut-cost-delay-oil-play-argentina/ )

The situation in Argentina highlights the underlying problem for the economics of shale oil and shale gas. Unconventional oil and gas fields have much higher costs than conventional ones. Tapping “conventional” oil and gas from permeable geological strata is cheaper in that the oil and gas flows underground and can be pumped out with less engineering. In contrast an “unconventional gas field” has to release the gas from impermable rock and therefore needs up to 100 more wells for the same amount of gas (or oil). A field must achieve economies of scale to have any chance of making a profit. It needs more activity underground to fracture the rock and it needs more activity on the surface to facilitate that. That is why it is more dangerous to the environment and public health – and also why it is more financially expensive. It requires more ongoing capital equipment too. Without a high gas (or oil ) price all of these activities cannot be made profitable.

Looked at in this way “unconventional oil and gas” is not the magical answer for peak oil (or later for peak natural gas) that it might have once seemed to be. To be long term viable the fracking sector requires three things: favourable geology, high oil and gas prices and easy and cheap credit. All three have proven elusive, making for disappointing results in all of the locations around the world where it has been tried. Unconventional gas is struggling to get off the ground outside of the USA and Australia. And in the USA, where it started, although it managed to get the credit to pay for the capital expenditure there are now grave doubts that a mountain of credit will ever be paid pack.

But let’s look outside of the USA too. Take Europe for example. In 2011 the international oil and gas industry and the Polish government thought Poland was going to be a major source of shale gas. 75 exploratory wells were drilled up to 2015 and 25 were fracked. The amount of gas recovered was one tenth to one third of what was needed for the wells to be commercially viable. Besides retreating from Poland, the industry has pulled out of nascent shale drilling efforts in Romania, Lithuania and Denmark, usually citing disappointing yields.

In the UK and Ireland too fracking is still stuck at the pre-exploratory stage, largely because of the rapid and powerful development of a movement of opposition. Although not definitive, a moratorium in Scotland and a “presumption against” fracking by planners in Northern Ireland, are political set backs for the industry. Yet even if the public and political opposition was not there, there would be reasons to doubt that fracking is viable in the UK. The doubt starts with the geology. While the British Geological Survey has produced maps of shale layers, and while it has been suggested that the carbon content might be there, the data is lacking for other key parameters, for example for rock porosity. In addition the shale in the UK has more folds and faults when compared to US fields. This might to lead to more earthquakes which would damage the wells – plus leading to a potential failure to achieve the pressure needed for fracturing if fracking fluid leaks into small faults when pushed underground.

Oil and Gas Prices

Now there are further doubts because of low and falling oil and gas prices. Here the issues are a little different for oil compared to natural gas on the one hand and for the situation in the USA as compared to other producing zones in the world on the other. That said, what all exploration and production companies are facing, whether in oil or gas production or whether in the USA or elsewhere, is that prices that are too low. It is proving difficult or impossible for most producers to make a profit given the costs of extracting and distribution. That has been especially noticeable for shale gas. Let us however first look at oil prices.

During the crash of 2007-2008 global oil prices crashed from a high peak but then recovered again. Between November 2010 and September 2014 there were 47 months in which oil prices were over $90 a barrel. This period of high oil prices can be described as being broadly reflective of supply and demand. On the demand side the global economy recovered, to a large degree stimulated by a massive credit-fuelled residential and infrastructure boom in China. This pumped up demand. On the supply side production from Libya and Iran was kept out of the world market because of the turmoil in Libya and sanctions against Iran. Thus, while there was some production increase from Saudi Arabia and, eventually, even more from Iraq, these increases were largely cancelled by Iran and Libya. Demand exceeded supply and prices remained high but the situation began to change in the autumn of 2014.

On the demand side the Chinese economy stalled while on the supply side production increased. OPEC as a whole was not the main source of that increasing production, and nor was Russia – the main source of increasing oil production was the boom in US shale oil. For reasons to be explored, production from the USA continued to soar even though prices fell and after a price rally early in 2015 prices continued to fall into 2016.

A similar downward trend has occurred around the world in natural gas prices – though in the USA they have been lower far longer – and certainly too low to allow for profitability.

In regard to gas the issues are somewhat different from oil because the market for natural gas is less globally networked. Natural gas markets are based on global regions and different gas prices in different parts of the world. Thus there is a north american gas market, a european gas market and a market in the far east. There are multiple long distance gas pipelines that are important economically and geopolitically. Wars and rivalries are fought over pipeline routes – this is a component in the Syrian conflict. However natural gas could not be transported so easily between continents – until recently, because now there is an infrastructure for sea transported liquified natural gas under development (LNG). Sea transported LNG begins to change things because it makes the market for natural gas more globally competitive.

At a risk of simplifying a varied picture natural gas prices in various areas have been stable at a low level or drifting downwards over the last two years and insufficient for profitability in a gas fracking sector. In both the USA and Europe natural gas prices are a half of what they were in 2014. In the USA this has been because of overproduction of gas, conventional and unconventional, with conventional production declining and being replaced and overtaken by unconventional production – as of late in 2015 however shale gas production too began to fall. For years production has been unprofitable in all but the best areas and in decline. Now it is in decline generally.

In Europe production decline because of depleting conventional gas fields has not prevented a fall in the gas price because demand has been falling too and this is likely to remain the case. Thus a recent report published by the Natural Gas Programme of the Oxford Institute for Energy Studies, concludes that European gas demand will not recover its 2010 level until about 2025. The decline in demand has been due to warmer winters but also due to low demand because of the low growth in manufacturing which has shifted to Asia, because of low population growth and because of energy saving measures too. At the time of writing it is being suggested that the competitive threat from the development of an LNG infrastructure will encourage Gazprom to change its pricing strategy to try to fight off future competition from sea transported supplies. In summary, it is highly likely that the gas price in Europe will remain low for a long time. If so, this completely undermines any remaining case for fracking for natural gas in europe, and particularly Britain.

At current gas prices all the exploration and production companies active in the UK and Ireland would struggle to make a profit. There are 4 studies of extraction costs of natural gas by fracking in the UK – by Ernst and Young, Bloomberg, Oxford Institute of Energy Studies and Centrica. All have maximum and minimum extraction costs. Current gas prices per therm are less than the minimum extraction cost in the lowest study. So for the industry to continue at all it has to assume that gas prices will rise in the future.

Low Gas price vs high extraction costs: Zachery Davis Boren, Greenpeace Energy Desk; August 2015 http://energydesk.greenpeace.org/2015/08/20/super-low-gas-price-spells-trouble-for-fracking-in-the-uk/

So what is the future for oil and gas prices? Of course the future is inherently uncertain – a President Trump might provoke any number of wars making America great again – it is difficult to see how Muslims could be banned from entry into the USA without that affecting oil and gas imports from Muslim countries. Or again heightened conflict between Iran and Saudi Arabia might escalate with massive consequences, and not just for the oil and gas price. In these and other conceivable situations, the more chaos the less companies will want to invest anyway. Whether prices are high, or low, if there is too much turmoil conditions will not favour new investment. But leaving aside extreme geo-political scenarios will prices go up or will they go down? If oil and gas prices rise will this be sufficiently and for long enough for unconventional gas to be developed sustainably in the narrow financial or business sense?

The rising price scenario

It is important to grasp the idea that a rising prices scenario is only credible in conditions where a proportion of the industry has been driven out of the business – which is the hope of the Saudi oil industry. What the Saudis would like to see is not only the US fracking companies driven to bankruptcy but the banks that fund them with badly burned fingers and unwilling to finance the industry any more. That said the Saudis too have limited pockets. Their current aggressive foreign policy has to be funded from somewhere and it is conceivable that they could lose the capacity to push the anti-shale agenda through to the bitter end.

If the oil price does bounce back the beneficiaries would be the survivors. There is a view then that the current low prices will eventually lead, not only to falling production in the future but to bankruptcies and capital expenditure cut backs both in the conventional and unconventional sectors. It would speed the decline of oil fields like those in the North Sea where investment is now being slashed. With declining supply, inventories will be sold off, the market will move back into balance…. and then further the other way – so that eventually demand again exceeds supply. Higher prices, possibly spiking, will encourage new investment and the fracking companies will surge back at the other side of the crisis.

What must however be assumed for this to happen is that at some point “growth will resume” because, over the last two hundred years, it always has. If growth resumes the demand for energy will revive in order to feed it – making more material production and consumption possible. Some economists argue that one factor encouraging a revival in demand ought to be the low energy prices themselves. Higher energy prices act as a drag on the economy so low energy prices should do the opposite – i.e. stimulate it. In a recent speech the chair of the US Federal Reserve, Janet Yellen, said that falling energy prices had, on average put an extra $1,000 in the pockets of each US citizen. It is assumed that this would encourage extra spending and thus extra income.

The falling or stagnant prices scenario

An alternative view is more sceptical about the revival of the global economy and of demand because of the high level of debt. In an economy where indebtness is low, falling energy prices probably would act as a stimulus for energy consumers. But will there be any or enough stimulus where the debt to income ratio is high? In an indebted economy windfall gains from reduced energy prices are likely to be partly used to pay off debts rather than being spent. A further issue is what will happen because of the way in which the finance sector has made itself vulnerable? It has channelled substantial credit to the energy sector – to exploration and development companies that now have difficulties paying this credit off? It certainly will not help in finding investment money to get fracking off the ground in the UK and elsewhere if it all ends in tears in the USA.

In the pessimistic scenario if the economy does not revive then there can be some scepticism that energy prices will revive too. This is the scenario in which deflationary conditions continue and even deepen. On this view the global economy is entering a long period of stagnation, decline and chaos. Some economists are describing how growth has slowed using descriptive phrases like “secular stagnation”. The fate of the Japanese economy from the early 1990s onwards gives grounds for comparison and concern. After a quarter of a century Japan has not escaped prolonged recessionary conditions. Because the global economy is highly indebted central banks have driven down interest rates to zero and now even below that. This has led to a bubble in asset markets but it has done little to spur generalised economic growth.

There could be a vicious circle here – without demand arising in a sustained growth process pushing up energy prices the profitability of the unconventional sector will never be sufficient to make future investment in that sector pay. In these circumstances future oil and gas production will not rise. Production will fall in the USA, especially as more of the identified sweet spots in the best plays are exhausted. In textbook supply and demand theory falling supply should eventually lead, ceteris paribus, to a rise in prices that justifies more investment and therefore more production. However “ceteris paribus” (other things remaining unchanged) does not apply in a stagnating or a declining economy. A declining economy is not one where private economic actors invest money in the hope of a future return because the necessary confidence and conviction about the future is not there. Purchasing power is hoarded, purchases are deferred where possible, debts are paid off where possible. These actions tend to intensify the deflation. If this is what happens, and it seems likely, it will make the problems of the shale gas sector even worse.

The Fracking Companies and the Finance Sector

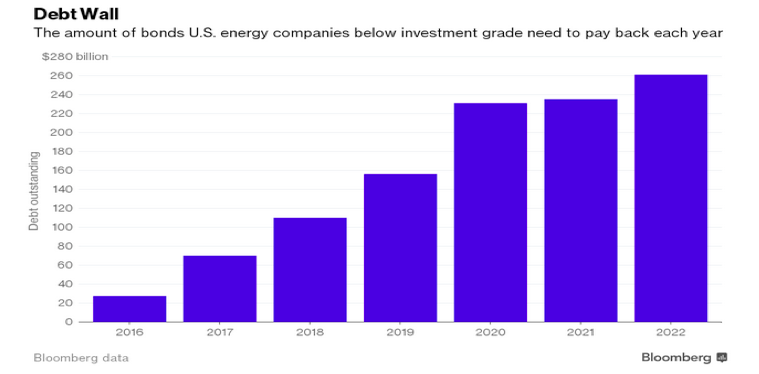

Before the current difficulties Wall Street made a fortune in fees arranging debt finance for the US shale sector. Investors who were “looking for yield” instead of the ultra low interest rates payable on government debt thought the way to find that yield was to pile their money into junk finance to fund the frackers. Despite the economic reality Wall Street encouraged the misinvestment. Now the wall of energy sector junk finance repayable in the future is huge. The further forward one goes the higher it is. How much of this debt will ever be repaid? And what will happen to those who lent it if it is not? Given what has already been said the long run ability of the sector to repay its debt seems highly questionable. How did it come to this?

Source: http://www.artberman.com/art-berman-shale-plays-have-years-not-decades-of-reserves-february-23-2015/

For several years prior to the crash of 2007-2008 the finance sector in the USA were knowingly giving loans to people with no income, no jobs and no assets. The people who organised this were doing so because they were earning fees on each loan arranged. What did they care about the virtual certainty that the loans would never be paid back? The crash was the inevitable result – the consequence of an ethical catastrophe. The banks had packaged the loans up into mortgage backed securities and sold them on so that someone else other than the originating bank carried the risk. Ratings agencies played their role in this crooked system and got fees rating securities that others called “toxic trash” as AAA. Meanwhile derivates contracts against defaults on these rotten securities were also sold even though it was not possible to pay up when the defaults happened – without being bailed out by the monetary authorities, as happened with AIG.

The Shale Bubble – toxic water, toxic air and toxic finance too

For several years after 2007-2008 shale was the next big money spinner – and the next ethical catastrophe for Wall Street. Just as it was blindingly obvious for years that sub prime would crash, but it was a nice money spinner at the time, so Wall Street has made a lot of money pumping up the shale bubble. All the evidence about health and environment costs have been ignored and the information about them suppressed. The information about the economics was ignored too. Of course, someone has to lose eventually but “while the music has played” there has been plenty of money for all sorts of players – petroleum engineers and geologists, PR companies, corrupt politicians, the companies supplying the pipelines, rigs and fracking gear. They had their snouts in the money trough and in many cases abandoned their ethics and their critical faculties while they were feeding.

Nor were investors looking closely enough at where they were going or at what they were funding. Even before the current price crash, many US fracking companies, just like those in Argentina and Poland, were struggling to make real profits yet vast quantities of money were channelled to them. Honest and astute observers who could see that the shale boom was a Wall Street induced bubble were ignored. One example was a report written by Deborah Rogers in early 2013 in which she drew attention to the difference between the reality and the message put out by the PR machine.

According to Rogers “Industry admits that 80% of shale wells ‘can easily be uneconomic.’ Massive write-downs have recently occurred which call into question the financial viability of shale assets and possibly even shale companies. In one case, assets were written off for more than 50% of the purchase price within a matter of months……publicly traded oil and gas companies have essentially two sets of economics. There is what may be called field economics, which addresses the basic day to day operations of the company and what is actually occurring out in the field with regard to well costs, production history, etc.; the other set is Wall Street or “Street” economics. This entails keeping a company attractive to financial analysts and investors so that the share price moves up and access to the capital markets is assured. “Street” economics has more to do with the frenzy we have seen in shales than does actual well performance in the field. With the help of Wall Street analysts acting as primary proponents for shale gas and oil, the markets were frothed into a frenzy. Boom cycles have the inherent characteristic of optimism. If left unchecked, such optimism can metamorphose into a mania such as we saw several years ago in the lead up to the mortgage crisis. (Deborah Rogers, “Shale and Wall Street” Energy Policy Forum 2013 http://shalebubble.org/wp-content/uploads/2013/02/SWS-report-FINAL.pdf)

Long before the price slide beginning late in 2014 the much hyped boom was not what it seemed. Roger’s article shows many parallels between the crazy and unethical excesses of Wall Street prior to the 2007 crash and what has been happening in the shale boom. As had happened with sub prime mortgages which were bundled up to become part of mortgage backed securities and then sold on – new kinds of financial assets were invented and sold to allow the unwary to invest their money in order as to “get a part of the action” and participate in the shale bonanza too. One bank instrumental in all of this was Barclay’s Capital, working together with a company called Chesapeake Energy. To help Chesapeake the Barclay’s financial wizards invented a structure called a Volumetric Production Payment (VPP). Rogers quotes a finance industry magazine, Risk, from March 2012.

“The main challenges in putting together the Chesapeake VPP deal were getting the structure right and guiding the rating agencies and institutional investors—who did not necessarily have deep familiarity with the energy business—through the complexities of natural gas production.”

The resulting financial assets were highly complex, off balance sheet, and as Barclay’s admitted the rating agencies had to be “guided” so that they could understand the complexities of the deal. (So much for the competence and independence of the resulting “rating”. ).

Production taking precedence over profitability (and over economic rationality)

The result was that current profitability took second place to an industry PR narrative about what was supposedly going to happen in the future as the shale companies grew and grew. Prior to the crash of 2007 bank employees were under pressure and being incentivised by bonuses to make as many loans as possible – even though many loans were unsound. Now the fracking company managers were being incentivised to produce as much product as possible even though they were losing money. The measure of the future dream was production growth rather than what it ought to have been – profitable production growth. The latter depended on whether that production growth was actually covering costs of production and it was not. It should be stressed again that this was happening before the current price slide. For example an analyst Arthur Berman looked at the financial figures for Exploration and Development Companies representing 40% of the US shale industry for 2013 and 2014 and found them to be powerfully in the negative. There was a $14 billion negative cash flow in 2014. (http://www.artberman.com/art-berman-shale-plays-have-years-not-decades-of-reserves-february-23-2015/)

Nevertheless the good news headlines about the production growth kept the share prices rising and the managers were on bonuses to make that production growth happen. Apart from the sceptics and the communities whose environments and health were under attack, the industry, the government, some naïve academics and Wall Street, all played their part in pumping up the dramatic narrative of the resurgent American Oil and Gas Dream. Eventually the USA would rival Saudi Arabia and more…becoming great again no doubt. As a more recent article in the Wall Street Journal explained:

“Markets have been waiting for U.S. energy producers to slash output during a period of depressed crude prices. But these companies have been paying their top executives to keep the oil flowing. Production and reserve growth are big components of the formulas that determine annual bonuses at many U.S. exploration and production companies. That meant energy executives took home tens of millions of dollars in bonuses for drilling in 2014, even though prices had begun to fall sharply in what would be the biggest oil bust in decades. The practice stems from Wall Street’s treatment of such companies’ shares as growth stocks, favoring future prospects over profitability. It has helped drive U.S. energy producers to spend more unearthing oil and gas than they make selling it, energy executives and analysts say.

It has also helped fuel the drilling boom that lifted U.S. oil and natural-gas production 76% and 31%, respectively, from 2009 through 2015, pushing down prices for both commodities. “You want to know why most of the industry outspent cash flow last year trying to grow production?” William Thomas, CEO of EOG Resources, said recently at a Houston conference. “That’s the way they’re paid.” (Ryan Dezember, Nicole Friedman and Erin Aillworth. “Key Formula for Executives Pay: Drill Baby Drill” http://www.wsj.com/articles/key-formula-for-oil-executives-pay-drill-baby-drill-1457721329)

The Euphoric Economy at Work – how to rip off manic investors

All of this raises the question of how, with profitability so low, this reckless show has managed to stay on the road for so long and still continues. A cynical answer would be to say that the function of Wall Street is to connect the greedy and stupid with people and institutions without scruples who will spend their money for them. For this to happen optimism must be generated at all times whether this optimism has any foundation or not. The study of bubbles is all about people who are able to swim in an ethical sewer oblivious to their environment. They are too “euphoric” or high on the prospect of making a lot of money to calmly calculate what is happening. Another word for this is mania. It helps to consider this as a period of collective madness like a mania – a period of collective excitement in which the capacity for ethical and other judgements are impaired.

In this collective insanity one can think of the money making calculations like this – if you buy the right to drill and are able to identify the geologically favourable “sweet spots” then at first the results are likely to be good. Instead of then drilling the less favourable locations and seeing your profits fall away you tell beautiful stories to another company with deep pockets enticed by the good news of the early success. So it is possible to sell the less favourable areas. Or maybe you sell the company, merging it with another. In this Wall Street (or the City of London no doubt) will come to your aid because it makes nice fees from mergers and acquisitions. The new owners then makes the loss. It is the buying company that then has to write down its balance sheet when it subsequently discovers that it was sold a mirage.

The stories about being duped are never told as loudly and plainly as the stories of the wonderful shining future that sell the fraud in the first place. That’s because managers do not like to speak loudly about their incompetence to avoid the embarrassment of admitting they were duped. It is usually possible to deny that it would have been possible for them to know what was happening and, after all, why should these managers care when it was other people’s money that they were losing? (The money of shareholders or bond holders).

But if the faith in the industry can be maintained then these kind of deals can at some time make the banksters and crooked production company bosses much more money than merely by drilling and fracking for shale gas or oil. Thus buying and selling drilling leases (bundled up together just like sub prime mortgages were) was a great money spinner for companies like Chesapeake. The greater the euphoria generated, the more money to be made. This is Deborah Rogers again:

“Aubrey McClendon, CEO of Chesapeake Energy, stated unequivocally in a financial analyst call in 2008: ‘I can assure you that buying leases for x and selling them for 5x or 10x is a lot more profitable than trying to produce gas at $5 or $6 mcf.’”

Eight years later Aubrey McClendon was dead. He had been charged on a federal indictment of bid rigging from late 2007 to 2012 and drove his car at high speed into a bridge. There was a strong suspicion that he had killed himself.

The madness of shale goes on. Wall Street and the shale companies are still managing to play the same game of passing the risk parcel to the bigger fools who will take the loss. If people can be persuaded to buy into the companies just before they go bust then the smarter and bigger players can get out. At the time of writing (March 2016) there are suspicions that the banks are orchestrating a rise in the price of oil in order to help the shale companies raise capital which will enable them to pay off the banks while letting “the suckers” take the fall. This led one analyst to describe the glut, not just of oil, but of stupidity.

“Even the experts are stunned by this unprecedented glut in stupidity of managers of other people’s money: “Billions of dollars of dilutive equity continue to roll in with seemingly no end in sight,” Houston-based oil investment bank Tudor, Pickering, Holt & Co. said in a research note.” (http://oilprice.com/Energy/Crude-Oil/In-Risky-Move-Wall-St-Backs-Shale-With-Nearly-10-Billion-In-Equity.html)

Ethical or Financial Bankruptcy – which is more fundamental?

It is common in economics to refer to markets becoming frothy at times like this. Commentators seek to find the fundamentals underlying the “froth” (perhaps better described as scum). But what are “the fundamentals” in this story? The really fundamental thing is not that this sector is financially bankrupt – it is that it is ethically bankrupt too. An ethically bankrupt sector is definitely not sustainable. Any economic sector that destroys the environment including the climate, assaults public health and then enlists government in a corrupting endeavour to write and use the regulations in such a way as to undermine the very possibility of resistance is corrupt to the core. An industry that destroys people’s health and environment and then settles in court on condition that people are bound to secrecy about what has happened to them, as is common practice in the USA, cannot be trusted to tell the truth. It does not surprise in the least therefore that the unethical business methods of this sector, as well as the unethical methods of its allies in finance, also rely on trickery and defrauding anyone stupid enough to invest their money in it.

What will happen in the USA will no doubt have a big impact for the future credibility of the fracking industry in the UK and elsewhere in the world. That story is not yet in its final chapter but what has happened in the USA is already a cautionary tale and we would be stupid to ignore it. Local authorities in the UK should be careful that they are not caught out picking up the environmental costs of a collapsing industry. It has already happened in the USA and Canada – the advantage of limited liability to an industry without ethics is that it enables it to pass the cost of clearing up to communities after bankruptcies.

“CBC News reported that falling gas and oil prices have prompted many smaller companies to abandon their operations in Alberta, Canada, leaving the provincial government to close down and dismantle their wells. In the past year alone, the number of orphaned wells in Alberta increased from 162 to 702. At the current rate of work,

deconstructing the inventory of wells abandoned just in the past year alone will be a 20-year task.” (Source: Johnson, T. (2015, May 11). Alberta sees huge spike in abandoned oil and gas wells. CBC News. http://www.cbc.ca/news/canada/calgary/alberta-sees-huge-spike-in-abandoned-oil-and-gas-wells-1.3032434 )

In conclusion – a mountain of debt that will never be repaid?

People might ask, if the future of fracking is so much in doubt then why bother to build a movement of opposition to oppose it? The answer can be expressed by adapting a famous quote by John Maynard Keynes. In the original Keynes says “the market can remain irrational longer than you can remain solvent”. The market can also remain irrational long enough to do a lot of damage. What this article has barely done at all is refer to what are called, in economics-speak, the “external costs” of fracking – the damages to climate, to local environments and to public health. Nor has this article examined the claimed benefits to employment and to local economies which are usually grossly overstated. There is now plenty of evidence about these things. What I have tried to do instead is to show that even in the narrowest of meanings of “economic” fracking does not make sense. A lot of damage is being done and there will be little positive to show for it. The ability to continue this destructive path is due to the legacy of political influence of the fossil fuel lobby in government and in the finance sector. The legacy influence has been strong enough to ignore and crush the opposition despite the damage. In the USA it can be argued that the fracking boom has been an irrational, unethical and ultimately unprofitable attempt to extend the lifetime of fossil fuels in order to keep the oil and gas industry in work, aided and abetted by Wall Street. It is an industry trying to secure a future for an influential network of professional and business interests that should, in truth, be being wound down – including the engineers, the university departments of petroleum geology, the regulators to name a few. A mountain of debt has been accumulated to perpetuate the illusion that these people have a future in which they can go on much as before – a mountain of financial debt that will never be repaid.

Stupidity has a knack of getting its way – Albert Camus

Sources and further reading:

On geological uncertainties: Mason Inman “Can Fracking Power Europe?”, March 2016 at http://www.scientificamerican.com/article/can-fracking-power-europe/

Charles Newbury, “Struggles to cut cost delay oil production in Argentina” Platts Oilgram News. August 17th 2015 at http://blogs.platts.com/2015/08/17/cut-cost-delay-oil-play-argentina/

Low Gas price vs high extraction costs: Zachery Davis Boren, Greenpeace Energy Desk; August 2015 http://energydesk.greenpeace.org/2015/08/20/super-low-gas-price-spells-trouble-for-fracking-in-the-uk/

European natural gas supply and demand: https://www.oxfordenergy.org/publications/the-outlook-for-natural-gas-demand-in-europe/ and https://www.oxfordenergy.org/wpcms/wp-content/uploads/2016/01/Gazprom-Is-2016-the-Year-for-a-Change-of-Pricing-Strategy-in-Europe.pdf

Oil Majors as a source of investment capital http://www.telegraph.co.uk/business/2016/02/12/oil-firms-urged-to-avoid-dangerous-investment-cuts /

Deborah Rogers, “Shale and Wall Street” Energy Policy Forum 2013) http://shalebubble.org/wp-content/uploads/2013/02/SWS-report-FINAL.pdf

Fragility of UK explorer’s finances: http://www.companywatch.net/wp-content/uploads/2016/01/oil-and-gas-smaller-cap-research-11-January-2016-final.pdf

Crisis in US Shale Sector: http://www.bloomberg.com/news/articles/2016-03-11/oil-boom-fueled-by-junk-debt-faces-19-billion-wave-of-defaults

Arthur Berman “The Miracle of Shale Gas and Tight Oil is Easy Money” http://www.artberman.com/the-miracle-of-shale-gas-tight-oil-is-easy-money-part-i/

http://www.artberman.com/art-berman-shale-plays-have-years-not-decades-of-reserves-february-23-2015/

Ryan Dezember, Nicole Friedman and Erin Aillworth. “Key Formula for Executives Pay: Drill Baby Drill” http://www.wsj.com/articles/key-formula-for-oil-executives-pay-drill-baby-drill-1457721329

“Energy in the economy”: Brian Davey Credo. Economic Beliefs in a World in Crisis Feasta books 2015. https://credoeconomics.com Chapters 32 and 33.

Jeff C

this is one of the best pieces ive seen on the state of the global energy system in years… and i read (or scan) dozens of them every week… not much is new to we few who are iniated on the subject matter, but its just so comprehensive and well-written… so, thanks.

it appears more and more that the Pentagon JOE report from 2008 was accurate all along… 2015 peak… 2020 decline.